This week, we confirmed that scammers are using CFPB employees’ names to try to defraud members of the public. We’ve heard from people, specifically older adults, who received phone or video calls.

We can’t say it enough – the CFPB will NEVER contact you and ask you for sensitive information or to pay money. This includes never asking you to pay an upfront fee or taxes, or telling you that you’ve won a lottery, sweepstakes, or class-action lawsuit. We also won’t ask you for personal or sensitive information before you can cash a check we’ve issued.

The latest phone and video scams may include:

A phone or video call or an email from an imposter claiming to be a CFPB or other U.S. government official

Messages or calls notifying you of an opportunity to participate in a class-action lawsuit, or that you’ve won a lawsuit or owe money you didn’t expect.

Being told you must first pay taxes or another upfront fee to collect the money. They may continue to find “reasons” for you to pay more fees or taxes. It is all part of the scam.

If you’re contacted by someone from the CFPB and want to confirm whether it’s real or a scam, call our consumer call center at (855) 411-2372 between 8 a.m. and 8 p.m. ET, Monday through Friday.

Scammers could reach out to you by phone, mail, email, text message/SMS, social media, messaging apps, or through other online channels. Scams can also occur in person, at home, or at a business.

Here are some common signs of a scam:

You’re told you’ve won a sweepstakes or lottery you didn’t enter, or that you’re owed money from a class-action lawsuit.

You’re asked to pay upfront taxes or fees – either foreign or domestic.

You’re being pressured to act now. Scammers don’t want you to take the time to do research or to think too carefully before parting with your money.

A person claiming to be a government official contacts you to confirm your windfall. The emails sent may even appear to be from real government email addresses, but if you look further, the email is not from a “.gov” email.

Criminals and scam artists may try different tactics or ways of reaching you, but here are tips for how to protect yourself or your loved ones from scams:

Don’t share sensitive information – Avoid sharing Social Security numbers, account information, or credit card numbers with people you don’t know.

Never pay upfront for a promised prize – If you’re told you must pay fees or taxes to receive a prize, it’s a scam.

If it sounds too good to be true, it probably is – If someone is trying too hard or pressuring you, you can always walk away.

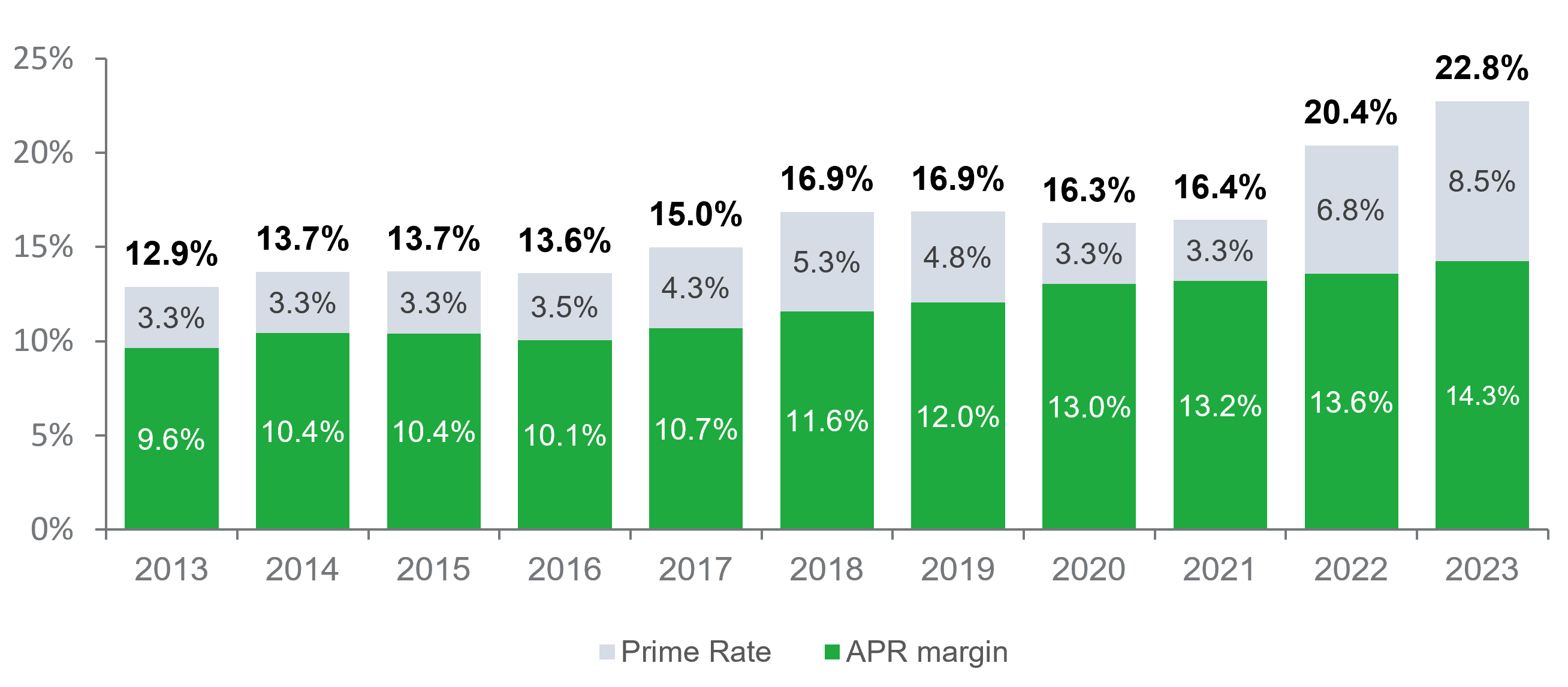

By some measures, credit cards have never been this expensive. For cardholders who carry a balance without paying it off in full each month, issuers generally charge interest based on annual percentage rates (APRs). In 2022 alone, major credit card companies charged over $105 billion in interest, the primary cost of credit cards to consumers. While the effects of increases to the target federal funds rate have received considerable attention, the average APR margin (the difference between the average APR and the prime rate) has reached an all-time high.

In this analysis, we show that higher APR margin drove about half of the increase in credit card rates over the last decade. In 2023, excess APR margin may have cost the average cardholder over $250. Major credit card companies earned an estimated $25 billion in additional interest revenue by raising APR margin. Increases to the average APR margin - despite lower charge-off rates and a relatively stable share of subprime borrowers - have fueled issuers’ profitability for the past decade. Higher APR margins have allowed credit card companies to generate returns that are significantly higher than other bank activities.

+

+

+

Credit card average APR margin is the highest on record.

Over the last 10 years, average APR on credit cards assessed interest have almost doubled from 12.9 percent in late 2013 to 22.8 percent in 2023 — the highest level recorded since the Federal Reserve began collecting this data in 1994. The APR on most credit card accounts can be viewed as being composed of the prime rate and the APR margin. The prime rate (a benchmark most banks use to set rates) represents a good proxy for banks’ funding costs, which have increased in recent years. But credit card issuers have also sharply increased average APRs beyond changes in the prime rate.

Nearly half of the increase in average APR over the last 10 years has been driven by issuers raising their APR margin. APR margin for revolving accounts is now at 14.3 percent, the highest point in recent history. More than half of issuers sent offers by direct mail with a higher APR margin in the third quarter of 2023 than on the same product the year before, according to our analysis of Competiscan data.

Figure 1: Average APRs on Accounts Assessed Interest and Average Prime Rate at Year End

+

+

+

+

+

Source: Federal Reserve

+

+

+

+

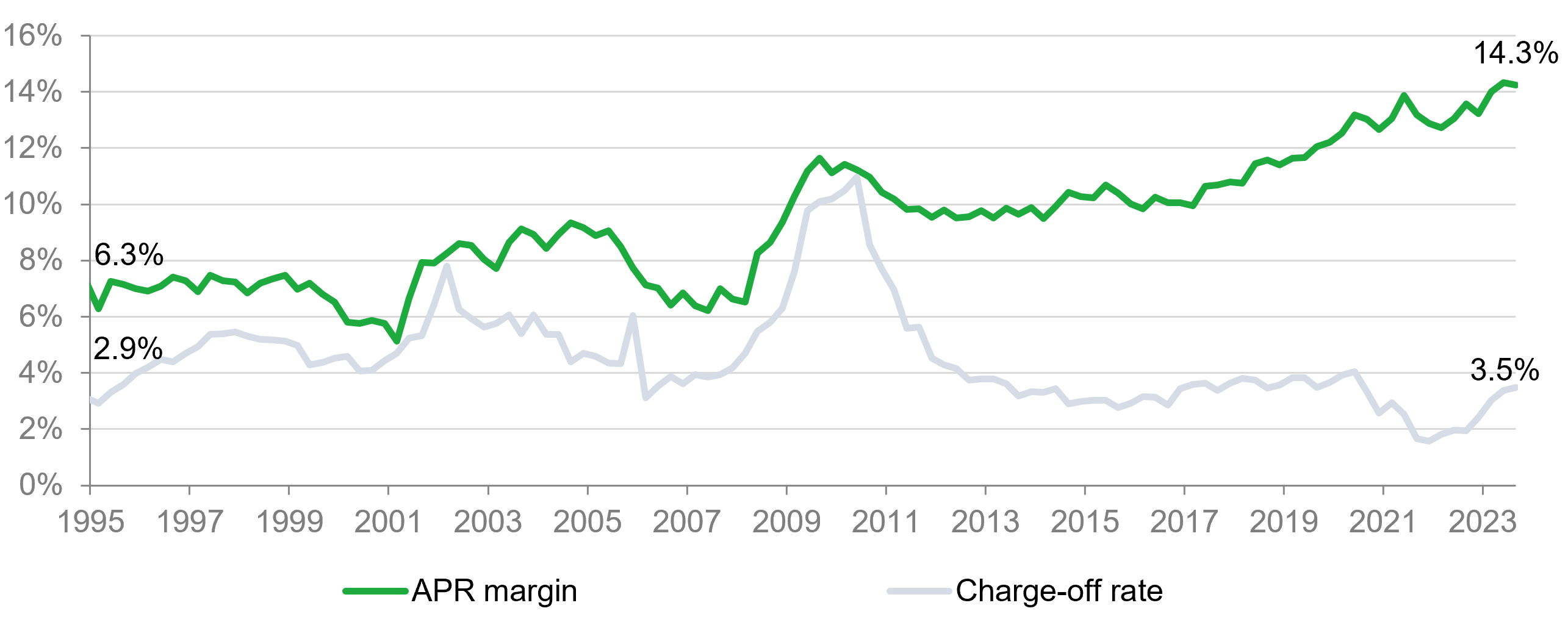

Higher APR margin has fueled the profitability of revolving balances.

Typically, card issuers set an APR margin to generate a profit that is at least commensurate with the risk of lending money to consumers. In the eight years after the Great Recession, the average APR margin stayed around 10 percent, as issuers adapted to reforms in the Credit Card Accountability Responsibility and Disclosure Act of 2009 (CARD Act) that restricted harmful back-end and hidden pricing practices. But issuers began to gradually increase APR margin in 2016. The trend accelerated in 2018, and it continued through the pandemic.

Over the past decade, card issuers increased APR margin despite lower charge-off rates and a relatively stable share of cardholders with subprime credit scores. The average APR margin increased 4.3 percentage points from 2013 to 2023 (while the prime rate was nearly 5 percentage points higher). As such, the profitability of revolving balances excluding loan loss provisions (the money that banks set aside for expected charge-offs) has been increasing over this time period.

Figure 2: Average APR Margin and Charge-Off Rate (Federal Reserve)

+

+

+

+

+

Source: Federal Reserve

+

+

+

+

Excess APR margin costs consumers billions of dollars a year.

In 2023, major credit card issuers, with around $590 billion in revolving balances, charged an estimated $25 billion in additional interest fees by raising the average APR margin by 4.3 percentage points over the last ten years. For an average consumer with a $5,300 balance across credit cards, the excess APR margin cost them over $250 in 2023. Since finance charges are typically part of the minimum amount due, this additional interest burden may push consumers into persistent debt, accruing more in interest and fees than they pay towards the principal each year — or even delinquency.

The increase in APR margin has occurred across all credit tiers. Even consumers with the highest credit scores are incurring higher costs. The average APR margin for accounts with credit scores at 800 or above grew 1.6 percentage points from 2015 to 2022 without a corresponding increase in late payments.

Credit card interest rates are a core driver of profits.

Credit card issuers are reliant on revenue from interest charged to borrowers who revolve on their balances to drive overall profits, as reflected in increasing APR margins. The return on assets on general purpose cards, one measure of profitability, was higher in 2022 (at 5.9 percent) than in 2019 (at 4.5 percent), and far greater than the returns banks received on other lines of business. Even when excluding the impact of loan loss provisions, the profitability of credit cards has been increasing.

CFPB research has found high levels of concentration in the consumer credit card market and evidence of practices that inhibit consumers’ ability to find alternatives to expensive credit card products. These practices may help explain why credit card issuers have been able to prop up high interest rates to fuel profits. Our recent research has shown that while the top credit card companies dominate the market, smaller issuers many times offer credit cards with significantly lower APRs. The CFPB will continue to take steps to ensure that the consumer credit card market is fair, competitive, and transparent and to help consumers avoid debt spirals that can be difficult to escape.

If you’re trying to correct inaccurate or incomplete information on your credit report, the process can feel overwhelming. The communications you receive from the companies involved can be confusing, and the CFPB has found some companies have not handled consumer disputes in compliance with the law.

The Fair Credit Reporting Act tells companies how credit reporting disputes should be handled. Some of the requirements apply to furnishers. Furnishers are the companies like banks, mortgage lenders, and credit card issuers that provide information that is included in credit reports.

According to federal law, if a consumer disputes directly with the furnisher the accuracy of information that’s been furnished to credit reporting companies, the furnisher is required to conduct a reasonable investigation about the dispute. After completing this reasonable investigation, the furnisher is required to “report the results of the investigation to the consumer” generally within 30 days.

We recently reported that CFPB examiners had found credit card furnishers were sending unclear notices to consumers at the end of dispute investigations. In some cases, these notices did not tell the consumer the result of the dispute investigation. Some of these notices didn’t even say whether the furnisher was going to correct the disputed information with the credit reporting companies. As a result, consumers were left in the dark about whether their problem was resolved.

After we conducted examinations of certain credit card furnishers and identified these problems, the credit card furnishers we examined revised their notices. The revised notices are more specific and clearly communicate whether changes were made to the consumer’s disputed account as a result of the dispute investigation.

If you have submitted a dispute directly to a furnisher, the response you receive should include the following information:

Identification of the account that you disputed;

A statement that the dispute has been investigated;

A statement that the dispute investigation has been completed; and

An explanation of the results of that dispute investigation.

If the furnisher’s investigation found that the information you disputed is accurate, the notice should clearly say this.

If the furnisher’s investigation found that the information you disputed is inaccurate or cannot be verified, the notice should say so and also state what corrections the furnisher is providing to credit reporting companies to fix the inaccuracy.

If you get a notice from a furnisher that doesn’t meet these minimum requirements, or if you remain confused about what the furnisher is going to do about your account, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372).

And if you haven’t already, you should submit a dispute about the account to the credit reporting companies as well. You have certain additional rights that only apply when you submit your dispute to a credit reporting company. You can get more information about how to submit a dispute generally on the CFPB website. We provide detailed instructions, addresses, and phone numbers for submitting disputes. Elsewhere on our website, we have provided some suggestions for what to do if your credit dispute is ignored or if you disagree with the results of the dispute.

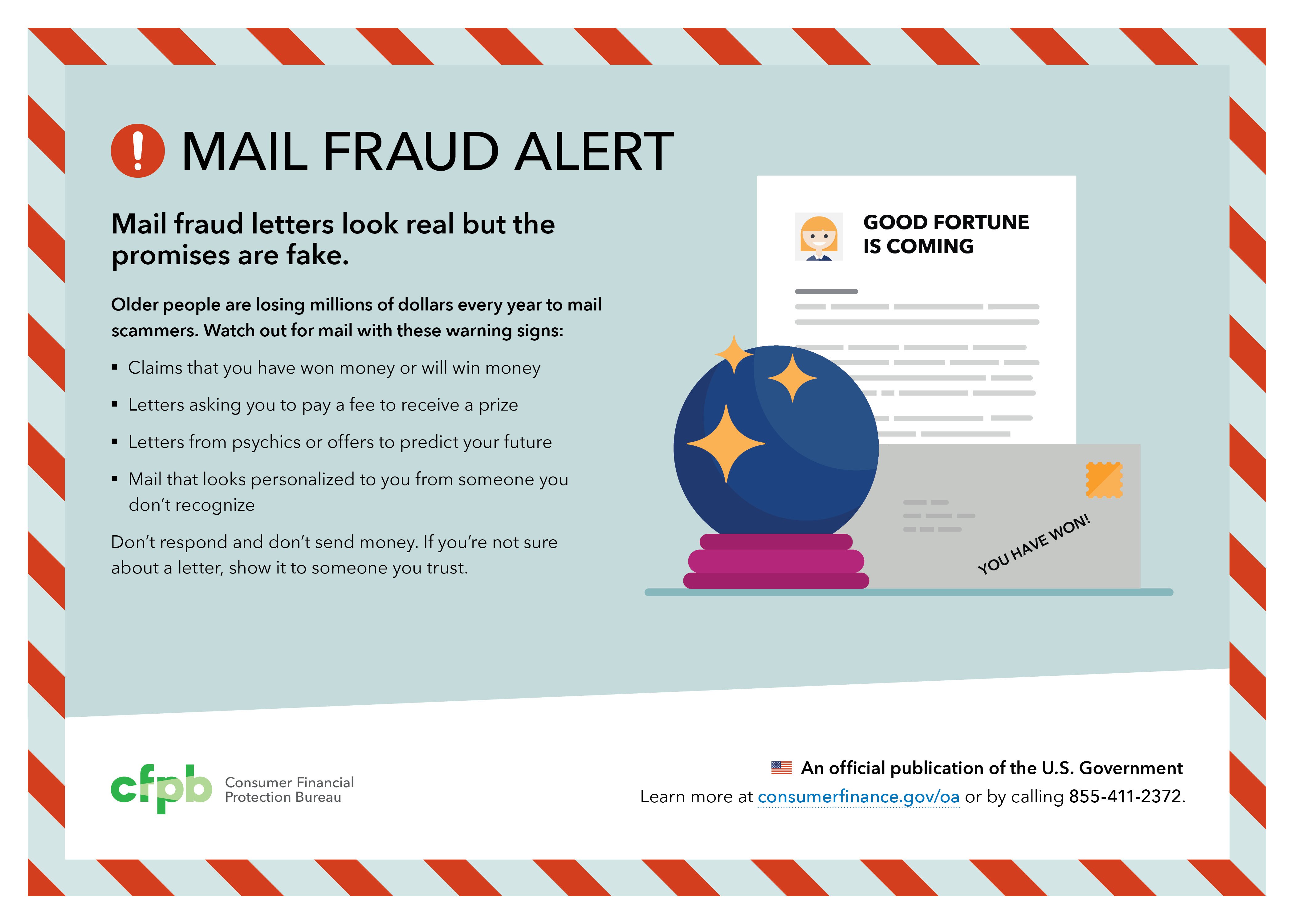

According to the Department of Justice, older people are losing millions of dollars to mass mailing fraud schemes, often by sending $20 or $30 at a time. These mail scammers use any means they can to convince victims to send them money, credit card details, and personal information like Social Security numbers. These offers often promise lottery winnings, gifts, good fortune, and other items for a fee, but never deliver anything of value.

To help warn older consumers, we’re working with Meals on Wheels America and other meal service providers to deliver new mail fraud alert placemats to seniors receiving meals nationwide. The placement gives consumers tips on how to spot suspicious mail and what to do to protect themselves.

In addition, this week we are partnering with several other federal agencies in a coordinated public education campaign to heighten awareness and educate potential victims and their families about mass mailing fraud schemes. It is our hope that this coordinated approach will create a lasting impact in the fight against financial exploitation.

To report suspicious mail, you can file a complaint online with the Federal Trade Commission (FTC). You can also call 1-877-FTC-HELP (1-877-382-4357) or 1-866-653-4261 (TTY). The FTC cannot resolve individual complaints, but your complaint could help law enforcement detect patterns of fraud and abuse. That may lead to investigations and eliminate unfair business practices.

For more information on identifying and preventing financial exploitation, you can download our Money Smart for Older Adults guide. To help financial caregivers protect family members and friends, we also offer easy-to-understand Managing Someone Else’s Money guides. For a variety of other useful financial information, visit our older Americans page.

Easy-to-remember guidelines help people reduce credit card debt

+

Take a short

+guideline like “don’t swipe the small stuff” and make it your own. You might

+just find that you’re better able to control your own credit card debt.

Have you ever looked at your credit card bill and

+wondered where all those charges came from? Or found yourself swiping your

+credit card for a purchase before you’ve had a chance to think about whether

+you really wanted to borrow money to pay for it?

+

Don’t feel discouraged – there are ways to get a

+better hold on your credit card use.

+

A recent study we commissioned found that following

+simple guidelines, or rules to live by, can help you lower your credit card

+debt, if you are a consumer carrying a month-to-month balance. The rules are

+designed to help you improve the choices you make with your credit cards –

+especially when you adjust the rule to live by to fit your personal financial

+situation.

+

We’ve created a worksheet to help you create and follow your own money rules

+to live by. Use the worksheet to:

+

+

Find areas where you

+ might use your credit card less often

+

Decide on a goal for

+ managing your credit card use

+

Create a rule to live by

+ for how you want to use your credit cards

+

Make a commitment to

+ yourself to act on your goal

+

Taking a close look at your small credit card

+purchases is one place to start to help gain control over your credit card

+spending. Then, you can create your own money rule to live by, such as using cash

+for similar small purchases in the future, to help make credit choices that

+work for you.

+

Using the worksheet to write down your goal will also

+help you stick to it.

+

Just like lane markers on a highway, your money

+rules to live by are guidelines that keep you moving in the right direction.

+You might have to speed some things up, slow down others, or change lanes from

+time to time, but your rules to live by can help you reach your financial

+destination.

When a catastrophe like Hurricane Maria, Hurricane Irma, or Hurricane Harvey happens, your world can be turned upside down. During these tough times, it may be difficult to know who to trust and where to look for guidance and assistance, as well as what financial steps to take as you begin recovering. These are a few organizations that can help immediately after a natural disaster:

The Red Cross can help you find aid and shelters. Local organizations will establish shelters and provide vouchers for meals, clothing and a limited amount of personal goods.

Start thinking about your financial obligations once you have addressed your most urgent needs, especially if you have experienced damage to your home or property. We have five steps you can take to help you secure your home and finances:

Contact your insurance company. If the storm damaged your home, car, or property and you have insurance, you can start the claims process by calling your insurance company. If you plan to claim damages related to flooding or storm damage, you should verify that you have the right kind of coverage. If you don’t have a copy of your insurance policy, you can ask for one. Ask for an electronic copy of your policy—receiving physical mail may be difficult following the flood. That will help you verify your coverage. If possible, take photos and videos of your damaged property. Documenting damage will help you with your insurance claim.

Register for assistance. Registering online at www.DisasterAssistance.gov, is the quickest way to register for FEMA assistance. If you are unable to access the internet, you can also call at 1-800-621-3362.

Contact your mortgage servicer. Talk to your mortgage lender right away and tell them about your situation. Damage to your home does not eliminate your responsibility to pay your mortgage, however your lender may be willing to work with you given the circumstances. If you don’t have your lender’s contact information, your monthly mortgage statement, or coupon book with you, you can search the Mortgage Electronic Registration Systems (MERS) or call toll-free at (888) 679-6377 to find the company that services your mortgage.

Contact your credit card companies and other lenders. If your income is interrupted or your expenses go up, and you don’t think you will be able to pay your credit cards or other loans, be sure to contact your lenders as soon as possible. Ask your creditor to work with you. Explain your situation and when you think you might be able to resume normal payments. It is important to make those calls before your next payments are due.

Contact your utility companies. If your home is damaged to the point you can’t live in it, ask the utility companies to suspend your service. This could help free up money in your budget for other expenses.

After contacting the companies related to your most urgent financial needs, take a look at your bills and set priorities—including your mortgage, rent, and insurance payments. Given the countless people experiencing distress from the flooding, contacting your creditors may be difficult. Be persistent and make every effort to reach them.

Additional resources

Forbearance. Depending upon the type of loan you have, your lender may be willing to temporarily reduce or suspend your payments; this is referred to as forbearance. To learn more, visit the U.S. Department of Housing and Urban Development (HUD). If you have student loans, ask your servicer if you qualify for a temporary forbearance. Federal student loan borrowers may be eligible for up to three months of forbearance.

Insurance settlement. Typically, your mortgage servicer will release a portion of the settlement money before work begins so you can hire a contractor. When the work is halfway finished, the servicer will typically release more money. The rest will be released once the job is finished and the home passes inspection.

While many people pull together during times of crisis, there is also an increased risk for scams and fraud. To avoid scams, you need to ask questions—lots of them. Questions will help you determine if something is too good to be true. If the person trying to sell you a product or service can’t or won’t answer your questions, this is a red flag that you might want to look for someone else to do business with.

Watch out for:

People who want you to pay up-front fees to help you claim services, benefits, or get loans.

Contractorsselling repairs door-to-door, especially when they ask to receive payment up front or offer deep discounts.

Con artists posing as government employees, insurance adjusters, law enforcement officials, or bank employees. It is easy to fake credibility and uniforms, so do not give out personal information to people you don’t know. Government employees never charge to help you get a benefit or service and will never ask for payment or financial information.

Fake charities. Normally, legitimate organizations do not have similar names to government agencies or other charities; so if they do, it may be a scam. Never give out donations over the phone.

Limited time offers. Anyone who offers you something and tells you that it is for a very limited time may be trying to pressure you into something that you could later regret. You should never be pressured to make a decision on the spot or to sign anything without having enough time to review it. Take your time, read and understand anything presented to you, and ask a trusted friend, relative, or attorney before acting.

Starting over requires a lot of hard choices. If you have been affected by disaster and want to make sure your financial records are secure, here is a checklist to help you consolidate all the information you need—including account numbers, personal records and financial records. Being prepared and knowing how to protect yourself can help you avoid scams and get back on your feet faster.

Person-to-person payment services and mobile payment apps have become part of everyday life for millions of people. Payment services and apps let you send money to people without having to write a check, swipe a card, or hand them cash. These services are becoming increasingly popular for things like paying a friend back for lunch, splitting the cost of rent with a roommate, or collecting money for a youth sports coach’s thank you gift.

Mobile payment services advertise to consumers that they provide increased security, ease of use, and speed over more traditional payment methods. However, many different forms and brands of these services exist—your friend may have told you about one mobile app, you may have used another to receive money from your brother, and your bank might have emailed you about their own app. You might have also heard about a different kind of service called a "mobile" wallet that lets you pay merchants. While payment apps all may appear to do the same thing, each of these services operates somewhat differently, and your experience with them may vary.

With the development of new payment methods come new risks. Mobile payment apps should have strong built-in protections to detect and limit errors, unauthorized transactions, and fraud. The federal Electronic Fund Transfer Act (EFTA) applies to a bank, credit union, or other provider’s mobile payment services, just like it does to an electronic bill pay service. Among other protections, this federal law requires these institutions to investigate errors reported by consumers. Other federal and state protections may also apply. Whatever service you end up using, keep the tips below in mind to make sure your money goes where you want it to and you receive money you’re owed.

Use caution when sending money to or receiving money from someone you don’t know

Scammers use mobile payment services to trick people into sending money or merchandise without holding up their end of the deal. For example, a scammer may sell you concert or sports tickets but then never actually give them to you. Or a scammer might purchase an item from you, appear to send a payment, and then cancel it before it reaches your bank account. Using mobile payment services with family, friends, and others you know and trust is the safest way to protect your money. The Bureau has more tips on how to avoid scams, as does the Federal Trade Commission (“FTC”).

Consider having your friend send you a request for payment first

If you’re sending money to someone for the first time, ask that they send a "request" from their app if that service is available. This helps ensure that you’re sending funds to the right person for the right amount. If the payment app does not have a request for payment function, consider sending a small, test payment to the recipient to confirm it is the right person before sending larger amounts.

Double check before you press send

A simple mistype can send money to the wrong person or in the wrong amount. Always double check the amount you entered and the person you selected to pay. Most payment apps use a username, phone number, or email address to identify payment recipients. Ask your recipient to be sure he or she has registered in the app with the information you intend to use to send them money.

Know how quickly you will receive your money—and how quickly money comes out of your account when you pay someone

Depending upon which mobile app you use and who sends you money, you may or may not be able to use money you receive immediately. In some instances, you may have to wait a few days to spend money you receive, even if the money shows up instantly in your app balance and you intend to spend the money within the same app. Many services let you transfer money to your bank account, and some will charge you a fee for the money to become available faster. For each app you use, find out how soon transferred money becomes available and then decide if that timing works for you.

Regardless of how quickly you can spend money you receive, when you send money via mobile apps, most payments you make get deducted from your balance immediately. You can sometimes put a "stop payment" on a check you’ve written, dispute a credit card charge, or cancel a bill payment. But new mobile payment services generally don’t have a recall or retrieval feature. For these reasons, again, it’s important to be certain you want to make a payment, for how much, and to whom before pressing send.

Set up your app to require a passcode, PIN, or fingerprint before making a payment

Most mobile payment apps allow you to set up a passcode, PIN, or fingerprint that you can use to authenticate yourself before making a payment. Setting up this feature helps to prevent anyone else that gets access to your mobile phone from making mobile payments from your account. In the event that your mobile phone is actually lost or stolen, be sure to notify your bank or payment provider.

Contact your bank or payment provider if you suspect an error

Under the federal law called the EFTA, banks, credit unions, and other financial institutions must investigate errors. In addition, a new Bureau rule explicitly applies the EFTA to prepaid accounts (including some payment apps) beginning in April 2019. If an erroneous transaction appears on your statement, you should notify your financial institution right away.

Many existing forms of payment offer protections in addition to those required by the EFTA. New mobile apps and forms of payment may not provide these same protections. That means it might not always be easy to get your money back if something goes wrong. Make sure you understand the protections and assurances your payment services provider offers with their service.

Similarly, as with any mobile app and before using the app, review the app’s privacy policy to understand what information about you is collected as you use the app and with whom this information may be shared.

Contact us if you encounter an issue with a bank or payment provider

The Bureau enforces the EFTA, which requires banks, credit unions, and other financial institutions to investigate errors. Congress also gave the Bureau the authority to hold companies that provide consumer financial products or services accountable for committing unfair, deceptive, or abusive acts or practices.

If you're having trouble with a payment service, you can submit a complaint online or call us toll-free at (855) 411-2372. If you have a question, and not a complaint, about payment services or other financial services, you can get answers to common questions through our Ask web tool.

The Bureau’s commitment to promoting safe and innovative payments

While the Bureau offers the tips listed above to help ensure your safety in the financial marketplace, people should be able to use new payment services with peace of mind and without fear of getting scammed or making honest mistakes. In concert with other regulators and industry stakeholders, the Bureau promotes the development of innovative payment services that offer people improved quality of life and that earn people’s trust and confidence.

Editorial note: This blog was originally posted on April 8, 2022, and has been updated on May 11, 2023.

Flooding, fire, drought, and other weather-related risks have always been a danger to property and consumer wellbeing. However, with the changing climate, these risks are increasing in intensity and frequency, impacting the likelihood of damage, cost of utilities, price of insurance, and potential resale value of homes.

A 2021 report by the First Street Foundation found that nearly 4.3 million residential homes across the country had substantial flood risk. For these properties, annual losses per property were estimated at $4,694, growing to $7,563 by 2051. Insurance can help minimize losses, however many homeowners, such as those in high-risk coastal areas in Florida, are facing rising insurance costs. Flood damage is not covered under most homeowners’ or renters’ insurance policies. In July 2022, when deadly floods hit eastern Kentucky, only 2.3% of homes in the area had government flood insurance, leaving many homeowners with insufficient resources to rebuild.

In other states, fire risk is a major factor, with an estimated 4.5 million U.S. homes at high or extreme risk, according to Verisk Analytics. Every property faces climate risks, however historically disadvantaged areas are disproportionately affected by heat and flood risk. For these homeowners, understanding climate risks is even more essential in order to take steps towards mitigation and plan for the future. Individual climate risks will vary based on location thus it is important to focus on the relevant risks for your area.

You have many factors to consider when deciding on a home: price, location, commute time, and schools, among others. It is time to add climate risks to that list.

Some major real estate websites already include flood risk and other climate risks in their listings. However, past flood damage can be hidden, costly to repair, and a sign of future risk. Before making an offer, look up a property’s climate risks using the resources below and check if your state has disclosure requirements for past flooding.

If a property is located in a FEMA high risk flood zone and you have a mortgage, you will likely be required to purchase flood insurance from the National Flood Insurance Program (NFIP) at additional cost, but it’s important to note that properties not in flood zones can still be at risk of flooding or other climate risks. On average, 40% of the National Flood Insurance Program (NFIP) flood insurance claims occur outside the high-risk flood areas. And in 2017, during Hurricane Harvey, thousands of properties not in flood zones ended up flooded, many of which did not have insurance to help with repairs. When looking for a home, carefully consider the costs and future availability of flood and homeowners insurance as well as needed resiliency or energy efficiency upgrades.

Flood is only one climate-related risk, and risks can vary greatly between properties. Investigate a potential home’s climate risk with some of these tools:

As a homeowner, it is important for you to know your climate risk so you can be better prepared for future costs and climate events. Often climate risks are undisclosed and only reveal themselves over time. Start by assessing the overall climate risk to your property, focusing on the most severe risks.

Next, evaluate how these risks may impact future insurance and utility costs as well as resale value. Examine your current budget and how it would be impacted by rising utilities and insurance costs. If your home is in an area that will get hotter or has high climate risks, these costs are likely to rise more than average. Additionally, if your property is severely impacted by climate risks, that could make it expensive or impossible to insure in the future, causing potential buyers to be wary.

Lastly, investigate options to mitigate and adapt to your climate risk. FEMA has advice on how to protect your home from flooding and wildfire. These can help but are no guarantee, thus additional insurance may be needed. To save on utility costs, consider energy efficiency or other improvements such as solar panels, improved insulation, and energy efficient windows and home appliances. New tax credits from the Inflation Reduction Act of 2022 can help decrease the total cost of certain improvements but watch out for potential scams or companies that promise unrealistic cost savings.

For renters

As a renter, you are not responsible for damage to a property due to a climate event, but you can still be vulnerable to physical harm, displacement, and loss of belongings. In addition, rising utility payments will impact renters either directly, if they are responsible for paying utilities, or indirectly, through increased rent.

As a real estate professional, you will need to comply with state and local disclosure requirements on climate risks. In addition, by providing information to the consumer about potential risks early, you can avoid negative outcomes for both the buyer and seller. In February 2023, the Mortgage Industry Standards Maintenance Organization (MISMO), a private industry standards setting body, published a Flood Risk Disclosure Guide to serve as a resource for lenders to inform consumers about flood risk.

In order to help your customer understand better their climate risk, you may want to familiarize yourself with the various climate risk tools available including:

*Although this blog includes links to private websites measuring and discussing climate risks, the CFPB cannot attest to the accuracy of these sources and encourages consumers to look at many sources when making decisions on climate risks.

The Consumer Financial Protection Bureau is committed to ensuring a fair, transparent, and competitive auto lending market, and we are taking action against sloppy servicing practices that cause harm. Some of these practices involve optional, add-on products that consumers can purchase when they purchase a car. For example, guaranteed asset protection (GAP) products offer to help pay off an auto loan if the car is totaled or stolen and the consumer owes more than the car's depreciated value.

The add-on product’s potential benefits apply only for specific time periods, such as four years after purchase, and only under certain circumstances. Auto dealers and finance companies often charge consumers all payments for any add-on products as a lump sum at origination of the auto loan, and they generally include the lump sum cost as part of the total vehicle financing agreement. Consumers typically make payments on these add-on products throughout the loan term, even if the product expires years earlier.

Our examiners have focused on the way servicers handle these add-on product charges when the loan ends before the add-on product’s potential benefits end. Such early termination may happen because the consumer pays the loan off early, often through refinancing, or because the consumer was delinquent in making payments and the servicer repossessed the consumer’s car. As we describe in a report released today, examiners found that servicers engaged in unfair practices by failing to request refunds from the third-party administrators for “unearned” fees related to one such add-on product, GAP, and failing to apply the applicable refunds to the accounts after repossession and cancellation of the contracts. At that point, the consumers did not have the cars that had been subject to the GAP product, and the product no longer offered any possible benefit to consumers. Examiners found that servicers later sent deficiency notices to consumers and reported balances to third-party debt buyers that included these inaccurate amounts in the deficiency balances owed by consumers.

In response to these findings, the servicers remediated impacted consumers and implemented additional controls to ensure they process add-on product refunds after repossession.

Miscalculating Refunds

CFPB examiners have also cited servicers for engaging in unfair acts or practices for miscalculating ancillary auto product refunds after repossession and attempting to collect miscalculated deficiency balances. For example, servicers incorrectly calculated refunds for extended warranty products or other products that had been financed through the consumers’ auto loans. The miscalculations reduced the refunds available to certain borrowers and led to deficiency balances that were higher by hundreds of dollars. The servicers then attempted to collect the deficiency balances. In response to these findings, the servicers conducted reviews to identify and remediate affected borrowers.

The CFPB will continue to scrutinize servicer practices to make sure that borrowers aren’t overcharged when their loans end early.

Today, the CFPB announced that it has approved an application that marks the first step for piloting disclosures for construction loans. Under this program, the CFPB authorizes parameters for in-market testing of alternatives to required disclosures. Real-world disclosure testing is often more accurate than lab testing, and this effort can help the CFPB by informing the need for possible regulatory changes.

The Independent Community Bankers of America (ICBA) applied under the program for a template covering the CFPB’s Know Before You Owe Disclosures. In particular, the ICBA asked to test certain adjustments to the existing mortgage disclosures in the unique context of construction loans, for which the CFPB’s disclosures were not primarily designed. The application noted that, in particular, many first-time homebuyers in rural areas build their homes instead of buying existing homes, and consequently, the challenges of using the current disclosures in the construction loan context may impact rural areas more acutely. The CFPB solicited comments on the ICBA’s application in February and made a decision to approve the template after reviewing the public feedback.

Individual lenders can apply for approval to test the alternative disclosures for construction loans. In deciding whether to approve individual lender applications, the CFPB will carefully evaluate a lender’s plan to test the effectiveness of these disclosures. The CFPB looks forward to reviewing any lender applications.

If you take a drive down the main road leading to most military bases in the country, you’ll likely see car dealerships lining both sides of the street. The CFPB’s prior research has shown that young servicemembers tend to take out auto loans soon after joining the military and carry more auto debt than their civilian peers. This isn’t altogether surprising. When many servicemembers finish basic training, their first duty station is often in an area where a car is needed to get around or leave the base.

Access to credit can be an important and valuable tool for servicemembers. At the same time, if a servicemember becomes unable to keep up with financial obligations, it can lead to adverse personnel actions such as a lost security clearance or potential discharge. Many servicemembers are young, first-time car buyers with limited knowledge of credit products and terms. Accordingly, they may be more likely to agree to products they don’t need or understand or receive loan terms that are not in their best interest. While we expect that lenders will treat all borrowers fairly and responsibly, lenders need to pay particular attention to how they treat servicemembers and their families.

CFPB research shows that by the age of 24, around 20 percent of young servicemembers have at least $20,000 in auto debt, which is nearly two-thirds of a young enlisted soldier’s typical base salary at that age. In comparison, only seven percent of civilians at age 24 have the same amount of auto debt while 71 percent don’t have any. Young servicemembers also generally have higher rates of delinquency and repossession, especially those who serve fewer than five years. Those who remain in service longer than five years have rates of delinquency that are virtually indistinguishable from civilians.

To better protect those who serve in our military, Congress passed the Servicemembers Civil Relief Act (SCRA). Among other protections, the SCRA provides specific safeguards for active-duty military members facing repossession of their cars. While we know that many lenders take following the SCRA seriously, over the past five years the Department of Justice (DOJ) has sued multiple lenders for violating the law in their auto repossession practices.

The CFPB recently released a bulletin outlining some concerns about auto loan servicing and wrongful repossessions with respect to all consumers. Additionally, it’s less costly to repossess a car because many lenders now use certain technologies that make it easier to locate the vehicle, including starter-interrupt devices, GPS locators, and license plate recognition. We’re concerned that the use of these technologies may disproportionally impact certain communities and we’re taking steps to better understand their impact, including potential privacy concerns.

We expect servicers, lenders, and repossession agents to adhere to the requirements under the SCRA, particularly when using new repossession technologies to ensure that servicemembers are treated fairly and that all applicable laws and regulations are carefully followed.

If you’re a servicemember and believe your SCRA rights have been violated, we encourage you to reach out to your local legal assistance office and file a complaint directly with DOJ. If you have more general trouble with a financial product or service, you can submit a complaint to the CFPB. Servicemembers are responsible for keeping our country safe from harm, and we’re committed to protecting them from unfair or illegal financial services practices.

Earlier this month, the Bureau of Labor Statistics released data regarding changes to the Consumer Price Index (CPI), which is one measure of inflation. The increasing cost of automobiles continues to be a major component of inflation, as many manufacturers face difficulties procuring chips that are a key component in cars and are therefore producing fewer new cars. While the chip shortage has caused new cars to grow more expensive, the price increase of used cars has been sharper. Data show that the CPI for used cars and trucks increased 40 percent since January 2021 while the CPI for new cars increased 12 percent. As car prices continue to rise, loan amounts are rising, and loan lengths are growing to make those larger loans seem affordable.

As a result, we expect that both the total amount of debt and the average loan size will continue to increase and that larger car loans will put increased pressure on some consumers’ budgets for much of the next decade. Auto loans are already the third largest consumer credit market in the United States at over $1.4 trillion outstanding, double the amount from 10 years ago and expected to grow further. We are also concerned that current high auto prices, especially for used cars, might create incentives for lenders to repossess cars more quickly than would have occurred before.

For many, their car or truck is essential to get to work or to do their work. Therefore, as the economic recovery continues, we will focus on ensuring a fair, transparent, and competitive auto lending market in the following ways.

Ensuring affordable credit for auto loans

When loans are affordable, consumers can repay the loan and continue to use their car. When loans are made at the edge of (or beyond) a consumer’s ability to repay, any economic disruption in the consumer’s life can result in repossession. Given the increase in loan amounts, the rising length of loan terms, and the uncertainty around the ongoing economic recovery, we will be closely monitoring lender practices and consumer outcomes. In particular, we continue to evaluate lending structures where lenders seem to rely on high interest rates and fees to profit even when consumers fail.

We are also concerned about loan-to-value (LTV) ratios in the auto loan market. While LTV ratios have dropped in the past year for consumers who already had cars due to high used vehicle prices, LTVs were climbing prior to the global vehicle shortage. We expect that trend to resume once price pressures abate. We will continue to monitor the market as pricing issues persist.

Monitoring practices in auto loan servicing and collections

The current economic recovery is uneven, and some consumers have been hit harder economically due to the pandemic. We want to ensure that incentives are aligned between servicers and consumers, that servicers are making accommodations available to all consumers and that servicer practices treat consumers fairly. We will also continue to work with our federal agency partners to ensure that the special protections offered to our servicemembers are followed and enforced.

Technology continues to shape auto loan servicing and collections, but with that comes questions about the effect on consumers. It is now less costly to repossess a car because many lenders require the use of some of these technologies. For example, some lenders require access to GPS locators so that they always know where a car is physically located, require the installation of technology that blocks a borrower who has missed even one payment from starting the car, or use license plate recognition (LPR) technology to find cars on repossession “hot lists”.

We are concerned that the use of these technologies may disproportionally impact certain communities, and we are taking steps to better and fully understand their impact, including privacy concerns associated with them.

Fostering competition among subprime lenders

Consumers with prime credit scores typically have many financing options, including borrowing directly from lenders. This provides them more leverage to negotiate interest rates. On the other hand, consumers with subprime credit scores often get loans indirectly through a smaller pool of lenders that operate exclusively through dealers or from buy-here-pay-here (BHPH) dealers that specialize in subprime lending. The result is less comparison shopping, fewer options, and less leverage to negotiate the interest rate.

CFPB research shows that the average subprime auto loan interest rate is between about 9 percent and 20 percent annually, depending on the type of lender. This variation has a large impact on consumers. Our report estimates that typical “shallow subprime” small BHPH borrowers would save around $894 over the life of a loan if they could reduce the interest rate from 13 percent, which is typical for such BHPH borrowers, to 9 percent, which is typical for bank borrowers with similar default rates.

We are looking to better understand potential barriers to competition in the subprime auto lending market that may drive these and related outcomes. We will continue to research auto lending policies and practices that may hinder a fair, transparent, and competitive market. And, we will work with our counterparts at the Federal Trade Commission and the Federal Reserve Bank Board of Governors to use our collective authorities to address issues in the market.

Given the steep rise in costs to purchase an automobile, it is critical that America has a well-functioning auto lending market. We will keep the public updated on changes to the market and the actions we are taking to ensure the market is working fairly for all Americans.

The Your Money, Your Goals financial empowerment toolkit is designed for organizations that help people meet their financial goals by increasing their knowledge, skills, and resources.

The pandemic has created uncertainty and anxiety in our country and around the world. This can be especially true for those who are unemployed or furloughed due to the coronavirus pandemic.

The Your Money, Your Goals financial empowerment toolkit has resources to help you evaluate your current finances and make decisions about your budget.

In this blog we highlight a few tools and handouts to help you make these tough decisions.

Paying your bills

If you are having trouble making payments, contact the companies you owe money to. Discuss your situation and options. Many companies have implemented special payment flexibilities for consumers experiencing hardship at this time.

Here are a couple tools to help you manage your bills.

Prioritizing bills

When you can't pay all your bills on time, this tool can help you prioritize which bills to pay first and helps you think through the impact of your choices.

Note: For expenses like utilities, phone and internet, mortgages, or insurance, many providers offer flexibilities to customers facing financial strain, and many are offering additional assistance during the pandemic. Check with your service providers, including utilities, phone and internet providers, mortgage servicers, landlords, and insurance companies. You can dial 211 and 311 to identify resources in your community.

This tool can help you keep track of when your bills are due and avoid late fees. For some bills, like credit cards, you may be able to adjust the bill’s due date by contacting your credit card company. For others, like rent, you may be able to split a large monthly payment into two smaller payments.

Reducing your spending and expenses may be an effective way to cover daily necessities. Having a clear picture of your spending helps you identify where you can reduce or better manage your money.

Spending tracker

Get an accurate picture of your finances. In normal circumstances, this includes getting a good sense of where your money is coming from (income) and where it’s going (expenses).While some of your expenses, like childcare or entertainment, may have stopped for the time being, you still need to make sure you can cover your basic necessities – food, housing, utilities, and phone.

This tool may spark ideas about how to cut costs and reduce expenses, so you can cover daily necessities. Some tips are commonly known, while others may be unfamiliar to people suddenly needing assistance.

It is important to understand that debt can represent a very real barrier to achieving goals and can be hard to face. But there are tools you can use to help you take control of your debt. Even small steps toward paying down debt can make a big difference in making it feel more manageable.

Debt log

This tool can help you to keep track of the debt you owe. After you get a clear picture of your debts, you may want to use the debt action plan to decide which debts to focus on first.

If a debt collector calls you, use this tool to make sure you’re asking the right questions. This tool will help you verify if the claim is valid, know how to dispute the claim if you do not owe the debt, and know what to do next if you do owe the debt.

Get prepared and read about your rights. This will help you avoid scammers who may pose as debt collectors to get you to pay on debts that you don’t owe.

While you’re working hard to make ends meet, scammers are working overtime to try to steal your money, your identity, or both.

You are the first line of defense when it comes to protecting your financial information from fraud or theft. The Spotting red flags and Protecting your identity handouts can help you be proactive about keeping your information safe.

It’s important to make time after you’ve figured out how you will be able to pay your bills and worked out repayment options to check your credit reports. Your credit reports and scores play an important role in your future financial opportunities.

Requesting your free credit reports

This tool walks you through the steps of requesting your free credit reports. Once you have them, use the Reviewing your credit reports tool to make sure your credit information is correct.

This tool can help you find incorrect information in your credit report. Errors can appear due to a mistake in the information provided about you or as the result of fraud or identity theft.

Sign up for the latest financial tips and information right to your inbox.

+

+

+

+

+

+

+

Find more information regarding COVID-19 from CFPB

We’re working to continuously update information for consumers during this rapidly evolving situation.

We will publish all COVID-19-related information and blogs to our resource page. Information should be considered accurate as of the blog publish date.

Whether or not you are among the millions of people affected by the recent Equifax data breach, there are several steps you can take to respond when your personal information is exposed in a data breach.

We outlined several identity theft tips for you last week. Since then, people have been asking many questions and we will continue to work to provide answers—or point people to other resources that may help make the situation clearer.

Free credit monitoring offered by Equifax

Equifax is offering a free monitoring service to anyone—not only those who are affected by this breach. Since this is a free service, you should consider signing up for this service, if it makes sense for you, by visiting equifaxsecurity2017.com.

Any time you are offered free credit monitoring, make sure you check for:

Trial periods

Fees

Cancellation requirements

Other restrictions, such as automatic renewals

Whether you are being asked to give your credit card, debit card, or bank account information

If you don’t give your credit card, debit card, or bank account information, that helps to avoid getting automatically renewed and charged for something that you expected to be free. This will also help to make sure you don’t face unexpected fees, charges, or other limitations.

+

+

+

Credit monitoring and arbitration

In the initial response to the data breach, people were concerned over an arbitration clause to enroll in Equifax’s TrustedID program for credit monitoring. Originally, this clause stated that claims and disputes against the company would be settled by arbitration, as opposed to in a court of law.

In an update for consumers, Equifax announced that it has removed the arbitration clause language from its terms of use for the credit monitoring product, called TrustedID Premier. With this change, the company has stated that anyone who enrolls in the company’s free credit file monitoring and identity theft protection will not waive their right to pursue legal action or join a class-action lawsuit concerning the cybersecurity incident or the TrustedID Premier product provided in response to that incident, should you choose.

Top 10 ways to protect your personal information from being misused

1.Review your credit report. You are entitled to a free credit report every 12 months from each of the three major consumer reporting companies (Equifax, Experian and TransUnion). You can request a copy from AnnualCreditReport.com.

2.Consider a security freeze. A security freeze or credit freeze on your credit report restricts access to your credit file. Creditors typically won’t offer you credit if they can’t access your credit reporting file, so a freeze prevents you and others from opening new accounts in your name. In almost all states, a freeze lasts until you remove it. In some states, it expires after seven years.

3.Set up a fraud alert. Fraud alerts require that a financial institution verifies your identity before opening a new account, issuing an additional card, or increasing the credit limit on an existing account. A fraud alert won’t prevent lenders from opening new accounts in your name, but it will require that the lenders take additional identification verification steps to make sure that you’re making the request. An initial fraud alert only lasts for 90 days, so you may want to watch for when to renew it. You can also set up an extended alert for identity theft victims, which is good for seven years.

4. Read your credit card and bank statements carefully. Look closely for charges you did not make. Even a small charge can be a danger sign. Thieves sometimes will take a small amount from your checking account and then return to take much more if the small debit goes unnoticed.

5. Don’t ignore bills from people you don’t know. A bill on an account you don’t recognize may be an indication that someone else has opened an account in your name. Contact the creditor to find out.

6. Shred any documents with personal or sensitive information. Be sure to keep hard copies of financial information in a safe place and be sure to shred them before getting rid of them.

7. Change your passwords for all of your financial accounts and consider changing the passwords for your other accounts as well. Be sure to create strong passwords and do not use the same password for all accounts. Don’t use information such as addresses and birthdays in your passwords. For more tips on how to create strong passwords read more from the Federal Trade Commission (FTC).

8. File your taxes as soon as you can. A scammer can use your Social Security number to get a tax refund. You can try to prevent a scammer from using your tax information to file and steal your tax refund by making sure you file before they do. Be sure not to ignore any official letters from the IRS and reply as soon as possible. The IRS will contact you by mail; don’t provide any information or account numbers in response to calls or emails.

10. If you are the parent or guardian of a minor and you think your child’s information has been compromised, here are some steps from the FTC you can take to protect their information from fraudulent use. If you think you or your child’s identity has already been stolen you can follow checklists and additional steps provided by the FTC to begin recovering from a case of identity theft.

If you have a debt in collection, it’s often a challenging time. You may be having a difficult time financially and that can be frightening. And if a debt collector contacts you about your debts, you may have concerns about whether the debt collector is legitimate, whether the debt is yours, or if the amount the collector is seeking to collect is accurate.

The Fair Debt Collection Practices Act makes it illegal for debt collectors to harass or threaten you when trying to collect on a debt. In addition, on November 30, 2021, the CFPB’s new Debt Collection Rule became effective. This rule clarifies how debt collectors can communicate with you, including what information they’re required to provide at the outset of collection about the debt, your rights in debt collection, and how you can exercise those rights.

Here are five key things to know about the new debt collection rule.

What is a debt collection validation notice?

When a debt collector first communicates with you, or shortly thereafter, they’re generally required to provide certain information about the debt. When the information is provided in writing or electronically, it is called a validation notice, and it will generally include information like:

Name and mailing information of the debt collector

Name of the creditor to whom the debt is owed

Account number (if any) associated with the debt

An itemization of the current amount of the debt that reflects interest, fees, payments, and credits since a particular date that you may be able to recognize or verify with records

The current amount of the debt as of when the validation notice is provided

Information about your debt collection rights including how to dispute the debt

This notice is meant to help you identify whether you owe the debt and whether the collector’s information about the debt is accurate. The notice must include a “tear-off” form that you can send back to the debt collector to dispute the debt or take other actions.

How often can a debt collector call me?

The Fair Debt Collection Practices Act (FDCPA) prohibits debt collectors from repeatedly or continuously calling you with the intent to harass, oppress, or abuse you.

Under the Debt Collection Rule, collectors are presumed to violate the law if they place a telephone call to you about a particular debt:

More than seven times within a seven-day period, or

Within seven days after engaging in a phone conversation with you about a particular debt

These call frequency presumptions only apply to calls placed by the collector to you. They don’t apply to text messages, emails, and other types of media. Those media have other limitations.

When can a debt collector report my debt to a credit reporting company?

There are certain steps debt collectors must take before they can report a debt to a credit reporting company. They must do any of the following:

Speak to you by telephone or in person about the debt

Mail a letter or send an electronic communication about the debt and wait for a reasonable amount of time, generally 14 days, in case it is returned as undeliverable

If the debt collector sends you a validation notice, it means that they’ve satisfied their requirement to contact you and, in general, can begin reporting the debt to credit reporting companies, provided they follow other laws about credit reporting.

Can a debt collector contact me on social media about a debt?

Debt collectors must follow certain rules if they contact you through social media, including:

Keeping the messages private – Their messages to you must be private and not viewable by the general public or by your friends, contacts, or followers.

Identifying themselves as a debt collector – If a debt collector attempts to send you a private message requesting to add you as a friend or contact, the debt collector must identify themself as a debt collector.

Providing a way for you to opt out of their communications – They must also provide you, in each message, a simple way to opt out of receiving further communications from them on that social media platform.

A “limited-content message” is a type of voicemail that a debt collector may leave for you that must include specific information. Limited-content messages must include:

A business name that does not indicate the caller is a debt collector

Telephone number(s) you can use to return the call

A request that you reply and the name(s) of who you can contact to reply

There’s also some optional information they can include, including suggested dates and time for you to reply. Voicemails that don’t follow these rules are not considered limited-content messages.

If you have a checking account, you might have to deal with an overdraft fee. An overdraft occurs when you don’t have enough money in your account to cover a transaction, and the bank or credit union pays for it anyway. Transactions include ATM withdrawals and debit card purchases as well as checks and ACH payments (such as online bill payments). Many banks and credit unions offer overdraft programs, and these can vary by institution.

Generally, if you overdraw your checking account by a check or ACH, your bank or credit union’s overdraft program will pay for the transaction and charge you a fee. By allowing your account balance to fall below $0, your bank or credit union will also effectively take the repayment right out of your next deposit. At most institutions, the overdraft fee is a fixed amount regardless of the transaction amount, and you can incur several overdraft fees in a single day.

Overdraft fees work a little differently for debit cards. Your bank or credit union cannot charge you fees for overdrafts on ATM and most debit card transactions unless you have agreed (“opted in”) to these fees. If you choose to opt in to debit card and ATM overdraft, you are usually allowed to make ATM withdrawals and debit card purchases even if you do not have enough funds at the time of the transaction. However, you will generally incur fees on transactions that settle against a negative balance later.

If you have not opted in to ATM and debit card overdraft, debit card purchases and ATM withdrawals will generally be declined if your account doesn’t have enough funds at the time you attempt the transaction. If you have not opted in, you will still be able to make ATM withdrawals and debit card purchases when you have enough funds at the time you attempt your transaction, and you will not incur an overdraft fee regardless of whether you have the funds to cover the transaction in your account when the transaction later settles.

Since opted-in consumers allow their bank or credit union to charge them fees in the event of an ATM or debit card overdraft, they generally pay more in overdraft fees than consumers who do not opt in. For example, in 2014 the CFPB reported that opted-in accounts are three times as likely to have more than 10 overdrafts per year as accounts that are not opted in. The CFPB also found that opted-in accounts have seven times as many overdraft fees as accounts that are not opted in. Take a closer look at how consumers are impacted by opting in to checking account overdraft.

Whether or not you opt in, you may still be charged fees for overdrafts on checks or ACH transactions. Still, deciding whether or not to opt in can be one of the most important decisions you make that affects the cost of your checking account.

Here are six steps you can take to reduce or eliminate overdraft fees:

Track your balance as carefully as you can to reduce the chance you’ll overdraft. Also, sign up for low balance alerts to let you know when you’re at risk of overdrawing your account. If you have regular electronic transfers, such as rent, mortgage payments or utility bills, make sure you know how much they will be and on what day they occur. Track the checks that you write and note when the funds are deducted from your account, so that you do not accidentally spend money you have already paid from your account. You also need to know when the funds you have deposited become available for your use.

Check your account balance before making a debit card purchase (or ATM withdrawal), and then pause to ask yourself if you any other payments coming up. Just because your account has enough funds when you’re at the checkout counter doesn’t mean you’ll have the funds later when the transaction finally settles. If you’ve recently written checks or made online bill payments that have yet to be deducted from your account, these could draw down your funds in the meantime, leaving you without enough funds to cover your purchase. Debit card overdraft fees can occur on transactions that were first authorized when there were sufficient funds to cover them, but took the account negative when the transaction settled.

Don’t opt-in. You can avoid paying overdraft fees when using your debit card for purchases and at ATMs by not opting-in, or by opting-out if you are currently opted in. This means that your debit or ATM card may be declined if you don’t have enough money in your account to cover a purchase or ATM withdrawal at the time you attempt a transaction. However, it also means you won’t be charged an overdraft fee for these transactions.

Link your checking account to a savings account. If you overdraw your checking account, your institution will take money from your linked savings account to cover the difference. You may be charged a transfer fee when this happens, but it’s usually much lower than the fee for an overdraft.

Ask your financial institution if you are eligible for a line of credit or linked credit card to cover overdrafts. You may have to pay a fee when the credit line is tapped, and you will owe interest on the amount you borrowed, but this is usually a much cheaper way to cover a brief cash shortfall.

Shop around for a different account. Find out about your bank or credit union’s list of account fees, or ask about them, then compare them with account fees at other banks or credit unions. Assess your own habits and what fees you may face. Consider penalty fees, such as overdraft and non-sufficient funds charges, as well as monthly maintenance, ATM surcharge, and other service fees. When comparing banks or credit unions, you might also want to consider factors such as the hours of operation, locations, access to public transportation, available products and services, and reputation for customer service.

Questions about overdraft fees or checking accounts?

Check out Ask CFPB, our database of common financial questions and answers.

Submit a complaint

If you have a problem with overdraft fees or any other financial products, you can submit a complaint online or by calling (855)411-2372

Prepaid accounts are one of the newer ways to store and spend your money. These include prepaid cards that you buy in stores or digital wallet accounts that you get online. With most prepaid accounts, you can spend the money you’ve loaded in advance for daily expenses or withdraw cash from an ATM. You can also have your income directly deposited into most types of prepaid accounts.

Not all prepaid accounts are the same. Each account has its own set of features, functions, and fees. To decide which prepaid account is right for you, it’s important to learn about your choices and compare the fees that will apply depending on how you use the account. Right now, it can be hard to compare accounts because each card displays fee information differently.

With our new rule you will get clear, upfront information about these fees so you can know before you owe and shop for the best deal. These comprehensive consumer protections included in the new rule take effect on Oct. 1, 2017.

The rule will also make sure prepaid accounts are safer to use -- whether you’re swiping at the register, shopping online, or scanning your smartphone.

Right now, if someone accesses your prepaid account and steals your money, your protections depend on the type of account you have and your cardholder agreement. Under our new rule, your money will generally be protected if your card is lost, stolen, or your account is wrongly charged. You’ll also be able to easily monitor your account for free.

If you’re a current prepaid card user, we have information and tips. You may have the right to choose how your employer pays you if offered a payroll card, or to choose how you get payments for some government benefits.

Today we are updating our mortgage

+servicing rules and expanding foreclosure protections for struggling borrowers

+and other homeowners.

+

Our mortgage servicing rules that

+became effective in 2014 require that the companies that collect and process

+mortgage payments, known as servicers, give troubled borrowers direct

+and ongoing access to servicing personnel, promptly credit payments, and

+correct errors on request. The rules also include strong protections for

+struggling homeowners, including those facing foreclosure.

+

Since we issued those rules, we have

+seen how they are working in the market, talked to those implementing and

+affected by the rules, and proposed updates to make these rules more effective. Today, we’re finalizing those proposed updates

+with some changes based on the comments we received. We’re giving servicers a

+full year (and for some changes longer) to implement these rules, but we want

+you to see now how they will help consumers, like you.

+

The rules include many changes, but below

+are several we want to highlight:

+

Help for struggling borrowers

+

Our rule updates the way servicers

+have to communicate with borrowers who have applied for loss mitigation. Loss

+mitigation is a process where the servicer works with a struggling borrower to try and

+find alternatives to foreclosure. For example, the updates require servicers to

+let borrowers know when their application for loss mitigation is complete. This

+is important because certain protections don’t begin until an application is

+complete. Servicers are often prohibited from conducting a foreclosure sale while

+they are in the process of reviewing a complete application.

+

These updates also require servicers to

+give the protections of the loss mitigation rules to certain borrowers more

+than once during the life of the loan. Currently, a servicer is only required

+to give those protections under the rule once to a struggling borrower. When

+the new rule goes into effect, certain borrowers who received help under the

+rule before may be eligible to get help again. Receiving the protections more

+than once is important for people who may experience an unexpected hardship, like

+the loss of a job or a debilitating illness.

+

Protecting successors in interest

+

The rule also provides

+more protections for successors in interest, individuals who didn't borrow the money originally but who acquire ownership rights to a home, often when the borrower dies or as

+a result of a divorce. The rule defines successors in interest broadly. It includes

+someone receiving the ownership interest when a property is transferred upon

+the death of a relative, as a result of a divorce or legal separation, through certain

+trusts, between spouses, from a parent to a child, or when a borrower who is a

+joint tenant dies.

+

The new protections require servicers

+to provide information to potential successors in interest about the documents

+that are needed to confirm their status. The rule also ensures that confirmed successors

+in interest are given access to many of the same notices and documents that

+the original borrower would receive.

+

Providing

+more information to borrowers in bankruptcy

+

Under our existing mortgage

+rules, servicers do not have to provide periodic statements or early

+intervention loss mitigation information to borrowers in bankruptcy. The new

+rules require servicers to provide statements to these borrowers in certain

+circumstances, with specific information tailored for bankruptcy, as

+well as a modified early intervention notice to let them know about loss

+mitigation options.

+

Our updates are finalized, but they won’t

+be in effect for a while in order to give servicers and others in the mortgage

+industry time to update their systems and to implement the new protections. If

+you are having issues with your mortgage, you can submit a complaint online or by calling (855) 411-2372.

Customers of Wells Fargo or any other bank or credit union should always closely monitor their accounts to make sure they don’t see unauthorized products or account activity. If you suspect that you had an unauthorized account opened, you should visit your local bank branch or call your financial institution. If you’re still having an issue, you can submit a complaint to the CFPB, either online or by calling toll-free (855) 411-2372.

The CFPB is requiring Wells Fargo to provide full refunds to consumers for the fees they incurred as a result of the bank’s illegal conduct, and affected customers are not required to take action to get a full refund.

The historic $100 million fine we imposed on Wells Fargo is in addition to the money the bank must pay back to harmed consumers. There were also fines from other government agencies. The CFPB’s large fine reflects the seriousness of these violations and sends the message to the bank and other financial institutions that this type of misconduct carries serious consequences.

It is also a good idea to periodically check your credit report. Get a free copy of your credit report at AnnualCreditReport.com. You can receive a free credit report from each nationwide credit reporting company once every 12 months.

In 2015, we published a report finding that 26 million Americans are “credit invisible.” This figure indicates that one in every ten adults does not have any credit history with one of the three nationwide credit reporting companies. The report also found that Black consumers, Hispanic consumers, and consumers in low-income neighborhoods are more likely to have no credit history or not enough current credit history to produce a credit score.

Today, we’re releasing a brief of the most significant findings, as well as a checklist of action items to help consumers who are new to credit or looking to rebuild.

Credit reports and credit scores play a crucial role in the lives of consumers in America. Fortunately, there are actions you can take to build credit.

Know what matters

Paying your bills on time, every time, is one critical step in building a good credit score. Also, don’t get too close to your credit limit. Experts advise keeping your use at no more than 30 percent of your total credit limit.

Find products that will help you to build your credit history responsibly

There are a number of existing products considered helpful in establishing or rebuilding credit histories, and provide you with the opportunity to practice making on-time payments that are reported to the credit reporting companies. Below is a list of common credit-building products to explore: